In his latest Coffee Break Briefing webinar, Frettens’ own Insolvency Guru Malcolm Niekirk looked at Avanti Communications and the implications that the case has for ‘drawing the line’ between what is considered a fixed or floating charge.

This is the summary of that briefing.

If you'd like to watch the webinar back, you can do so below, if not, read on for our summary...

Quick Links

- What a fixed charge is

- What a floating charge is

- Why IPs need to categorise charges

- How to categorise charges

- Implications of avanti communications

What is a fixed charge?

A fixed charge is a security for a loan. The lender has ownership rights over the property, including the right to sell if the borrower is in default.

The borrower has the right to their property back on repayment. Until then, the borrower cannot sell the property unless they have the lender’s consent.

What is a floating charge? And how is it different?

A floating charge is a charge over a class of asset, typically something like ‘all present and future stock in trade’ or ‘all the assets, property and undertaking of the company.’

A floating charge allows a borrower to do anything with the charged property, despite it being security for a loan, without express permission from the lender (until the lender withdraws their consent). In particular, the borrower does not need the lender’s consent to sell property charged by a floating charge (as long as the sale is in the ordinary course of the borrower’s business).

Withdrawal of consent is known as crystallisation. It converts the floating charge into a fixed charge. That gives the lender all the rights, powers, and property interest that they would expect to have from any other fixed charge.

However, the priority of a charge is set by its category at the time it is created. So crystalised charges still have their original floating charge priority.

More in depth definition of both fixed and floating charges can be found here.

Why do Insolvency Practitioners need to categorise charges?

The main reason why you need to know if a charge is a fixed or floating is to assess its priority.

These are, in brief, the main rules:

- Charges do not often rank equally among themselves (unless set by a priority agreement)

- Legal charges rank over equitable charges

- Fixed charges rank over floating charges

- Where the category of two charges is the same:

- Older charges rank over newer ones

- Registered charges rank over unregistered

A deed of priority, an agreement entered into between the lenders with the consent of the borrower, can change the priority of a charge.

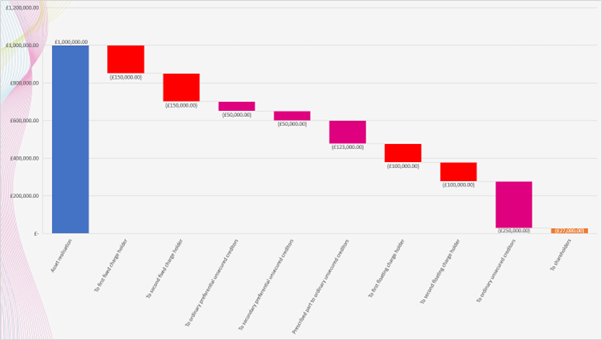

Here’s an example of how funds may be distributed in order of priority. The blue bar on the left hand side is money you have, hypothetically, received from the realisation of the asset:

Some floating charges are qualifying floating charges. Those give their holder the right to appoint an administrator of the company.

For more on this, again, please refer to my previous briefing here.

How to categorise charges

To categorise a charge as fixed or floating is a binary decision. But there isn’t a clear dividing line between fixed and floating charges.

Avanti Communications was a High Court decision. It was all about where that line should be drawn. The judge reviewed all previous decisions in great detail and gave general guidance on where the line should be drawn; not just for this specific case.

Earlier cases, like Brumark and Spectrum Plus, emphasised the issue of ‘control’ when drawing the boundary between fixed and floating charges. They suggested that the lender would need a high degree of control for a charge to be fixed.

Implications of Avanti Communications

The facts of Avanti were not very unusual.

A debenture contained the usual battery of fixed and floating charges. In particular, it claimed fixed charges over:

- a satellite,

- some Earth-based hardware, and

- permits for those.

Crucially, the lending documents did restrict Avanti from disposing of those assets. They were quite detailed restrictions, but also, in many cases, quite loose restrictions. The court assumed that they were genuine and were intended to be obeyed by the borrower.

The line was drawn here somewhere between the lender having lots of control and the lender having some control. The High Court thought this was enough control for the lender to have a fixed charge.

The key takeaways

- Fixed assets can easily be caught in the fixed charge in a debenture

- Current assets are likely to be caught only by floating charges

- In most bank debentures, these are likely to be fixed charges:

- Land and buildings

- Plant and machinery

- Goodwill

- IPR

- Contacts, licences, etc.

- And these floating charges:

- Book debts

- Stock

- Cash at bank

The bad news

Avanti is a High Court Decision and, as a House of Lords decision, Spectrum Plus out-ranks it.

Meaning that, although Avanti gives much needed clarity and is very recent, it could be overruled in future.

Upcoming events

Thanks for reading this summary…

You can read and watch back our previous Coffee Break Briefings here.

Our Third Annual all-day in-person Insolvency Conference will be taking place in 2024. Date and venue to be confirmed.

Specialist Insolvency Solicitors

If you have any questions after reading this article, please don’t hesitate to get in touch with our bright and experienced team.

Call us on 01202 499255, or fill out the form at the top of this page, for a free initial chat.

Comments