In his latest Coffee Break Briefing, Insolvency expert, Malcolm Niekirk discuss Boardroom Bust-ups, exploring the processes involved and the practical solutions available.

In case you missed it, you can read a summary and watch the video here.

Boardroom disputes are common.

Disagreements between directors, executives or shareholder can escalate. If not addressed, they can disrupt the business, cause stalemate, and can become terminal.

What does a typical scenario look like?

A familiar situation might involve a business that is fundamentally sound. However, there may be just one serious problem emerging with the potential to overwhelm the business.

Examples might be:

- Directors unable to agree on important business decisions

- Shareholders similarly unable to agree

- Legal disputes that take up time, money and attention

- A contract that no longer benefits the business but is hard to exit

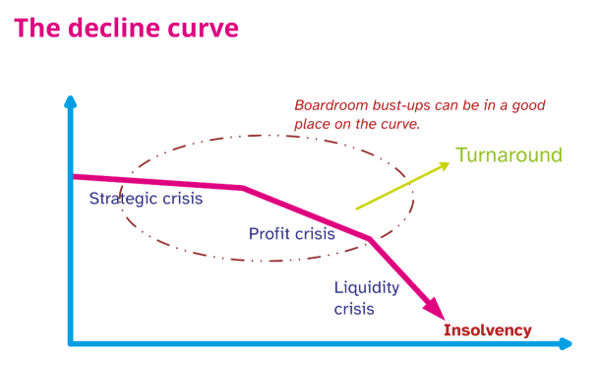

The decline curve and boardroom bust-ups

The decline curve shows the stages a struggling business may go through as problems arise. It typically begins with a strategic crisis, where underlying issues first emerge. If left unresolved, this can progress into a profit crisis, followed by a liquidity crisis and ultimately insolvency.

The earlier stages, particularly between the strategic and profit crises are critical. At this point, businesses often have more alternatives available, which may include a genuine opportunity to recover. Acting early can make the difference between a successful restructuring and a far more limited set of outcomes later on.

It’s usually best to remove the root cause of a problem. However, this is not always realistic when it’s a boardroom bust-up. The solution may be too complex, or too costly. In those cases, it may continue to drag the company down.

One common solution is to transfer the business to a new company. This allows it to continue operating without the burden of the existing issue.

Can transferring the business to a new company help?

Transferring a business to a new company can be an effective way of separating the viable operation from the problematic element. This can enable the business to continue trading.

It is often a pragmatic solution where resolving the underlying issue directly is not possible at a manageable cost.

What are some of the benefits and risks of transferring a business?

There are several potential advantages to transferring a business into a new company. It can be quicker and less expensive than negotiating a settlement to the conflict, while also offering more certainty.

Key benefits may include:

- Speed

- Less cost

- Greater certainty

- The end of the dispute

However, disadvantages can include:

- Reputational damage

- Disruption to the business

- Litigation risk

Careful planning and early advice are essential to manage these risks effectively.

Part of that planning is for the business valuations that the company and its advisors will need. It will be very important to show that the price the new company pays to buy the business is a fair one.

What are the insolvency options?

In many cases, transferring the business to a new company will lead to the insolvency of the previous corporate owner. A specific formal insolvency procedure might be a key component of the plan. The most common procedures to consider are likely to be pre-liquidation sales, liquidation pre-pack sales and administration pre-pack sales. Each option comes with its own requirements and challenges.

Pre-liquidation sales

A pre-liquidation sale requires compliance with the Companies Act 2006, including sections 175, 177 and 190. Directors must disclose any personal interest in the transaction. Both board and shareholder approval will usually be required. Constitutional documents, such as the articles of association, and perhaps a shareholders’ agreement, may add further requirements.

Depending on the circumstances, and the nature of the underlying dispute, it may be impossible to secure the approvals needed for a pre-liquidation sale.

It is also important to consider which third-party consents are needed, such as from regulators, landlords or contractual counterparties.

Another issue is the ban on reusing a business name following liquidation. Under section 216 of the Insolvency Act 1986, liquidation puts directors under an automatic five-year ban on using the same or a similar trading name. There are limited exceptions. The most useful comes from purchasing the business from an insolvency practitioner with proper notice to creditors. But that can’t be used in a pre-liquidation sale.

There’s also the risk of a legal challenge from the aggrieved party. Where there is a boardroom bust-up, there will be an aggrieved party. They may be able to argue a claim in tort, such as ‘conspiracy to procure a breach of contract’ or the ‘Marex tort’ (or some other claim). That might allow them to sue the new company and its directors, as well as the old company and its directors.

Sale following liquidation

This might be described as a liquidation pre-pack. Appointing a liquidator needs resolutions from directors, members and creditors. That can be difficult if the dispute involves parties with a decisive vote on those resolutions.

A sale following liquidation has a number of possible advantages over a pre-liquidation sale.

For example, TUPE rules (the Transfer of Undertakings (Protection of Employment) Regulations 2006) apply differently in liquidation. This can make it easier for the business to make changes that affect employees.

For another, the ban on reusing a business name following liquidation is easier to side-step. The directors can probably use the exception that comes from purchasing the business from an insolvency practitioner with proper notice to creditors. However, that exception comes with some critical time limits. They can be difficult to comply with, and the business may have to close for a few days to do so.

Pre-packaged administration business sales (administration pre-packs)

Administration pre-packs are often a preferred option for sorting out boardroom bust-ups.

To enter administration, the company must be (or be likely to become) unable to pay its debts, and the purpose of administration must be reasonably achievable. This may include rescuing the company as a going concern, achieving a better outcome than liquidation, or making distributions to secured or preferential creditors.

There are several routes into administration, including appointment by the company, or its directors, appointment by a qualifying floating charge holder, or appointment by court order.

In potentially contentious cases, appointment by court order may be the safest option. Technical errors in appointing by other means may result in the administration being declared invalid.

How can a business resolve a boardroom dispute?

Boardroom disputes can be highly disruptive, but they do not have to result in failure.

Insolvency procedures are not necessarily a sign of failure. They can be the best way out.

There are several procedures to choose from, each with its own advantages, risks and practical considerations.

An administration pre-pack sale, while expensive, may be the best solution in some cases.

As with so many business difficulties, timing is critical. The earlier a business addresses a problem, the more options it will have available. And the better its chances of preserving value and achieving a positive outcome.

Insolvency Coffee Break Briefings

Thank you for reading the summary for this Coffee Break Briefing. You can watch the full, detailed webinar here. If you have any questions after reading this article, please don’t hesitate to get in touch with our bright and experienced team. Call us on 01202 499255, or fill out the form at the top of this page, for a free initial chat.

Never miss out on one of Malcom's FREE briefings again, and sign up to receive updates here.

Comments