In his latest Coffee Break Briefing webinar, Frettens’ own Insolvency Guru Malcolm Niekirk looked at agreeing creditor’s claims.

This presentation was Part 1 (of 2), where he predominantly looked at voluntary liquidations with a particular emphasis on CVLs rather than MVLs.

You can sign up for Part 2 at the bottom of this article.

This is the summary of that briefing.

If you'd like to watch the webinar back, you can do so below, if not, read on for our summary...

Quick Links

Stopping Litigation

This is really about the insolvency moratorium. All insolvency procedures have one, but the detail is different in different procedures.

Not all types of litigation and enforcement are treated the same way in the moratorium, and I’ll look at some of the detail that applies to voluntary liquidations.

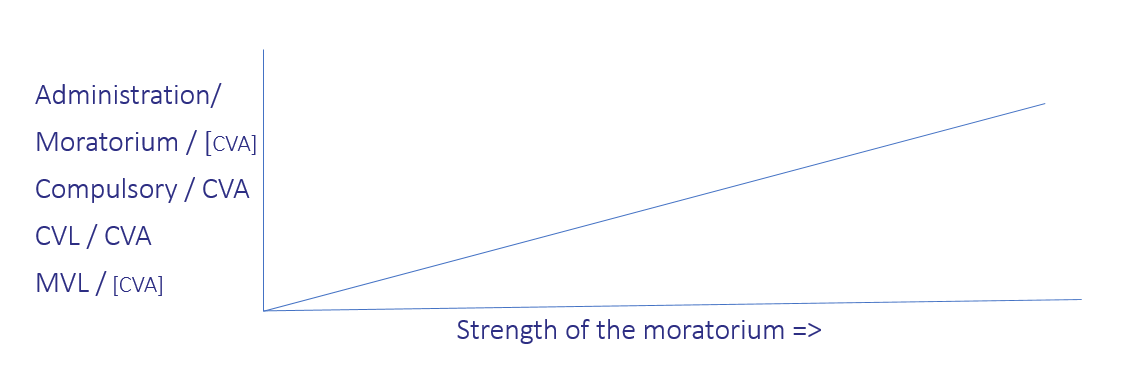

The strength of each type of moratorium

This graphic is intended to be a representation on how different procedures have moratoriums with different strengths.

Administration, and the new moratorium procedure give the greatest protection. It’s rather weaker for compulsory liquidations, weaker still for CVLs, and MVLs are the weakest of all.

That makes sense because, in an MVL, you should pay the creditors in full, so you shouldn’t normally need anything to hold them at bay.

CVAs are a flexible insolvency tool. When drafting the proposal you should write the terms needed for the moratorium, typically, it tends to be very similar to the liquidation moratorium.

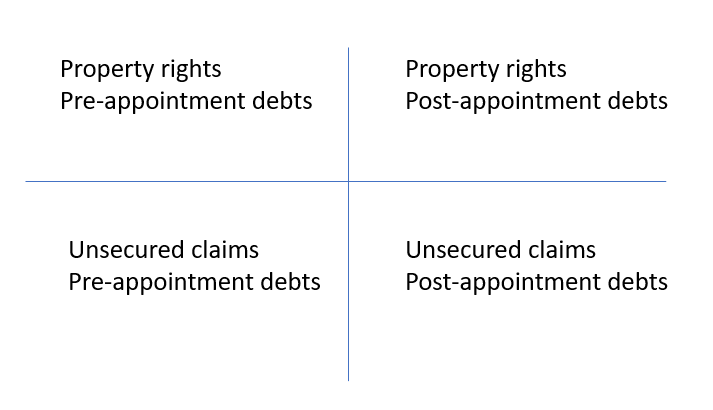

A quadrant of claims

I found it useful, when looking at the way that the moratorium works and the different types of enforcement, to put claims into a four-quadrant matrix.

The horizontal cut here is between property rights, which are always in a privileged position (think, for example, of the rights that secured creditors have, by comparison with unsecured claims), and a vertical cut between pre and post appointment debts.

Who are the secured creditors?

These creditors have property rights:

- Mortgage lenders

- Leasing companies

- Retention of title creditors

- Landlords

They may seek to recover post appointment debts

- Mortgage interest

- Hire rental

- The value of retention of title goods used or sold on

- Rent for the premises

Typically, a secured creditor has the right to limit their losses by taking back their property. But, in an administration, not always.

Some of the detail for voluntary liquidations

There are two takeaway points on the importance of the r6.14 (s100) notice for the moratorium that you’ll have in a liquidation.

- Firstly, the r6.14 notice should refer to the proposed resolution to wind up the company.

- Secondly, make sure that the notice goes out to any enforcement agents, bailiffs etc. that may be acting for creditors (in addition to the creditors themselves).

Staying creditors’ claims

In voluntary liquidations, there is no automatic stay on litigation.

In practical terms, most creditors taking debt collection action against a company that goes into liquidation will normally stop as soon as they hear about the liquidation.

If you need the court to order a stay, you can very often get it. There is an automatic stay on litigation in compulsory liquidations that brings all current litigation to a halt and stops new litigation. There’s a similar, discretionary, stay when a petition is running.

In a voluntary liquidation, as liquidator, you can ask for a compulsory liquidator’s powers. This gives the court a discretion to order a stay if useful to do so.

This is more likely for CVLs, and less so for MVLs. However, even in a CVL, you’re unlikely to get a stay which prevents a property owner from enforcing their property right. You’re more likely to get a stay that prevents an unsecured creditor from continuing their litigation

When can the court refuse to grant a stay on litigation?

Here are some examples where the court might allow litigation to continue:

- When the bust company is only one of several defendants

- Disclosure of evidence from the company’s records may be important

- When there is a claim against an insurer

- Third Parties (Rights against Insurers) Act 2010 allows the creditor to sue the insurance company. Very often there can be good reason for them also to sure the bust company at the same time.

- When there is a dispute, better settled in court, over

- Quantum; or

- Liability

- When it’s a property owner protecting their ownership rights, for example:

- A landlord forfeiting the lease

- A mortgage lender repossessing

- A leasing company seeking a protection of property order

Enforcement of court judgements in voluntary liquidations

The statutory rules apply where a creditor:

- Brought debt collection litigation before the company went into liquidation,

- Got a judgement, and

- Is trying to enforce that judgement, and

- A liquidator is appointed after enforcement has begun.

At what point is the line drawn to stop them from keeping the enforcement that they started?

The basic rule is:

To be allowed to keep it a judgement creditor has to ‘complete’ enforcement before either:

- Winding up starts; or

- (If earlier) they have notice of the proposed WU resolution (e.g. in your r6.14 notice).

When is enforcement ‘complete’?

- Once goods have been sold (or a charging order on them is made)

- Upon receipt of an attached debt (making the final ‘third part debt order’ does not ‘complete’ the enforcement)

- And, against land, upon:

- Seizure

- Appointment of a receiver

- A charging order being made

What if enforcement has started, but not finished?

Suppose the judgement creditor started, but didn’t complete enforcement against goods…

The key date would be when the bailiff got notice that the bust company is in liquidation; or (if earlier) if it was calling an EGM to pass a WU resolution.

And, suppose they hadn’t sold the goods by then.

In this situation, they have to pass to you the goods (and any money they’ve received). But, they have a charge on the goods, and money, for their costs.

The court has a discretion to disapply this rule.

What about in a compulsory liquidation?

In a compulsory liquidation, once a winding up petition is running, any attachment, distress (CRAR) and execution of a judgement (charging orders, court receivership, etc.) become void.

This applies to non-court procedures too, such as CRAR by landlords, HMRC, etc. or HMRC ‘hold’ & ‘deduction’ notices (taking money from the bust company’s bank account).

In a voluntary liquidation, the court has a discretion to apply these rules (using ss112, 126 & 130), to set aside this type of enforcement action.

Valuing creditor’s claims for voting purposes

Creditors often don’t realise that the value of their claim is likely to be assessed more than once over the history of the voluntary liquidation.

The claim will be valued:

- Pre-appointment (statement of affairs and the appointment decision procedure)

- Post appointment for the decision on the basis for your remuneration, and other decisions

- When you pay dividends (proving the claim)

Different rules apply for valuing their claim for voting purposes and for proving purposes. For voting purposes, the rules are in r15.31-15.33 and, for proving for a dividend, the rules are in r14.

Who decides on entitlement to vote?

It is the convener or chair of the decision procedure (r15.33(1)) who decides whether to admit the claim or not (and for how much).

In a CVL appointment, that may well be the director rather than you.

If you decide (or advise) on whether to admit, you have the choice to:

- Admit the claim in full (if it is ‘plainly and obviously good’),

- Reject it in full (if it is ‘plainly and obviously bad’),

- Admit and reject certain parts, or

- Mark it as objected to (if there is a question, or doubt)

- The creditor can then vote on it and there may be an appeal in court

There are pre-conditions. Before a creditor can vote:

- The creditor must have delivered a proof (r15.28(1)(a))

- There are time limits – r15.28(1)(b)

- And supporting evidence, if demanded (and necessary) (r15.28(4))

- And any proxy being used (r15.28(2))

Calculating the value of the claim for voting

You should start with the figure that is claimed in the proof. If you admit that figure in full, that of course is the value for voting purposes.

- For fully secured debts – the value is nil (r15.31(4))

- For partly secured debts – the value is that of the unsecured part (r15.31(5))

- For unliquidated or unascertained debts, the value is nil*, unless:

- The chair / convener puts an estimated minimum value on it; and

- Admits it to vote (r15.31(2))

*This is different from a voluntary arrangement. In a VA, the ‘default value’ for such claims is £1.

Creditors can vote on less than the admitted value; and split the way they vote (r15.31(9)).

Contingent claims

Contingent claims are not expressly covered by the rules. So, if you’ve got one:

- First decide whether to admit (or reject) in whole or part, or mark as objected to.

- (The decision on liability)

- Then assess if it is also unliquidated or unascertained

- (The decision on quantum)

- (You have to do this if the claim is not admitted in full, even if it is objected to)

- Very often at least part of it will be unliquidated or unascertained

- You don’t have to put a minimum value on it

- But you should, if reasonable to do so.

Creditors have 21 days to appeal to court.

Summary

This is Part 1 (of 2) of ‘agreeing creditor’s claims’, where we covered stopping litigation, and valuing for voting purposes.

In Part 2, which will be my next Coffee Break Briefing, I’ll look at valuing for dividends, contested claims, creditor’s appeals and more.

That webinar is set to take place on Monday 10th July. We’ll send the invite out to the insolvency list shortly (you can sign up to emails here.)

Lastly, I’d like to remind you to try out our tailored Retention of Title Flowchart here.

Specialist Insolvency Solicitors

If you have any questions after reading this article, please don’t hesitate to get in touch with our bright and experienced team.

Call us on 01202 499255, or fill out the form at the top of this page, for a free initial chat.

Comments